When you first step into the world of insurance, the language can sound like an entirely different dialect — full of terms, abbreviations, and phrases that seem confusing. Whether you’re buying health, life, or auto insurance, understanding the basic terms can make all the difference in choosing the right policy and avoiding misunderstandings later on.

This guide breaks down the most important insurance terms in a simple and friendly way, so you can feel confident when talking to agents, comparing plans, or reading policy documents.

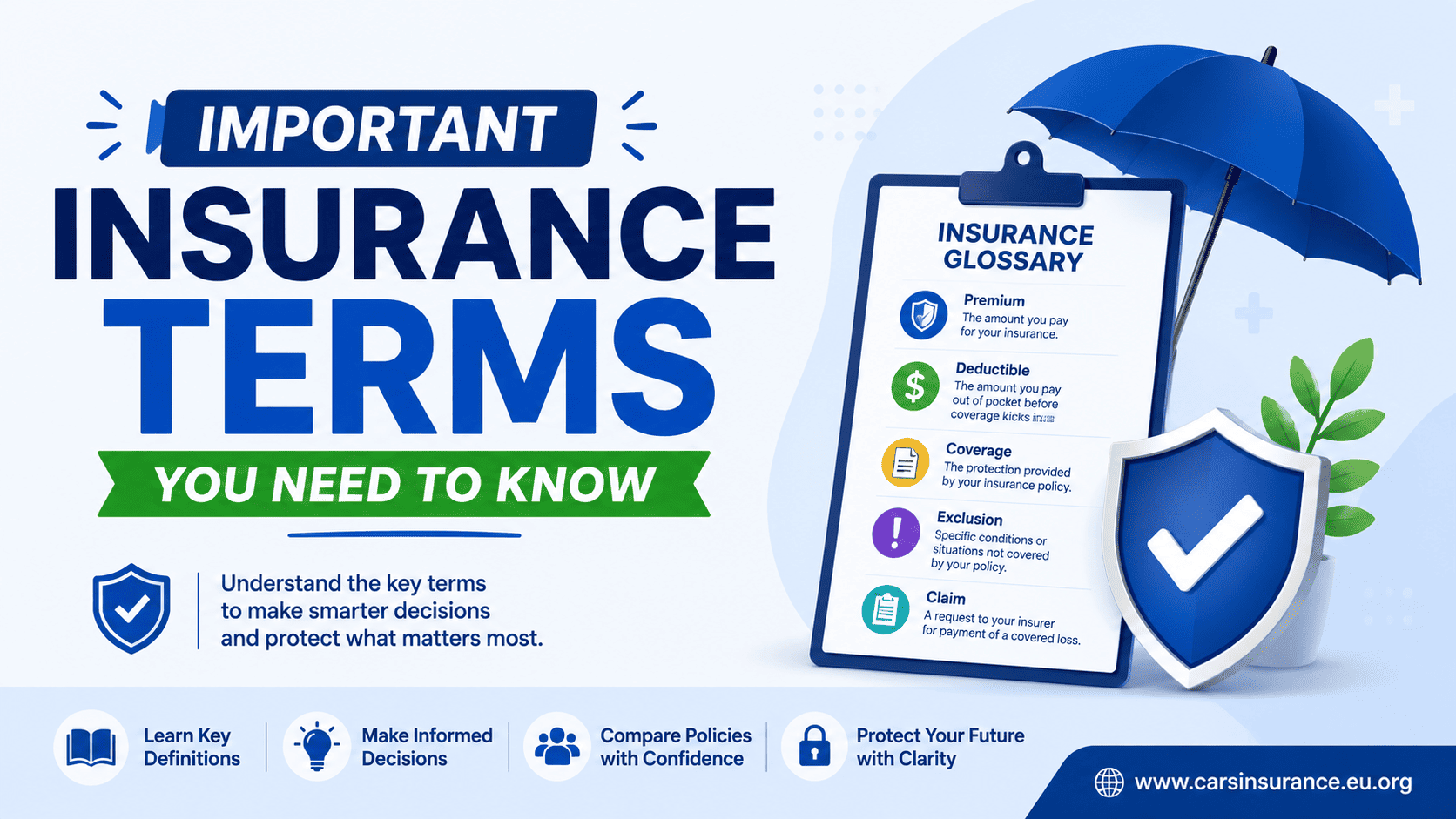

1. Premium

This is the amount you pay for your insurance — typically every month, quarter, or year. Think of it as a subscription fee that keeps your insurance coverage active.

💡 Example:

You might pay $120 per month for your health insurance plan. That’s your premium.

Premiums vary depending on several factors: your age, location, health condition, and the level of coverage you choose.

2. Deductible

A deductible is how much you pay out of your own pocket before your insurance company starts to cover costs.

💡 Example:

If your health insurance has a $1,000 deductible, you’ll pay the first $1,000 of your medical bills before your insurer begins to help.

A higher deductible usually means a lower premium, but it also means more risk for you if something happens.

3. Copayment (Copay)

A copay is a fixed amount you pay for a specific service after your insurance starts covering you.

💡 Example:

You might pay $20 each time you visit your doctor or $10 for a prescription.

Copays are common in health insurance and are separate from your deductible.

4. Coinsurance

Coinsurance means you and your insurer share the costs after you’ve paid your deductible.

💡 Example:

If your plan has 20% coinsurance, and a hospital bill costs $1,000, you pay $200 and your insurer pays $800.

Coinsurance helps spread financial responsibility between the insured and the insurer.

5. Coverage Limit (Policy Limit)

This term refers to the maximum amount your insurance company will pay for a covered loss.

💡 Example:

If your car insurance has a $50,000 limit for property damage, your insurer will only pay up to that amount — anything above it comes from your pocket.

Always check your policy limits carefully, especially for liability and health coverage.

6. Beneficiary

A beneficiary is the person who receives the insurance payout in case something happens to you.

💡 Example:

In life insurance, you can name your spouse, child, or even a trust as your beneficiary.

Choosing the right beneficiary ensures your loved ones are financially protected.

7. Exclusions

Exclusions are things your insurance won’t cover. This could be certain health conditions, types of accidents, or specific activities.

💡 Example:

A travel insurance policy might exclude injuries caused by extreme sports like skydiving or scuba diving.

Always read the “exclusions” section carefully before signing any policy.

8. Underwriting

Underwriting is the process insurers use to evaluate your risk before issuing a policy.

They’ll look at factors like your age, occupation, health history, driving record, or even credit score to determine whether to offer coverage and at what price.

9. Claim

A claim is a formal request you make to your insurer when a covered loss happens.

💡 Example:

If your car is damaged in an accident, you file a claim to ask the insurance company to pay for repairs.

Filing claims promptly and providing the right documentation can help ensure faster payouts.

10. Grace Period

A grace period is the extra time your insurer gives you after a missed payment before canceling your policy.

💡 Example:

If your payment is due on the 1st of the month, you might have until the 15th to pay without losing coverage.

This is especially important for health and life insurance policies.

11. Rider (Endorsement)

A rider is an add-on or modification to your insurance policy that provides extra benefits or changes coverage terms.

💡 Example:

You might add a critical illness rider to your life insurance so that you receive a payout if diagnosed with a serious condition like cancer.

Riders are a great way to personalize your policy for your specific needs.

12. Policyholder

The policyholder is the person who owns the insurance policy — the one responsible for making payments and managing the coverage.

💡 Example:

If you buy a health insurance policy for your family, you’re the policyholder, even though the plan covers everyone.

13. Lapse

A lapse occurs when your policy expires or becomes inactive due to non-payment.

If your coverage lapses, you might lose protection and have to reapply — often at a higher rate.

14. Subrogation

Subrogation is when your insurer pays you for a loss and then seeks repayment from the party responsible.

💡 Example:

If another driver causes an accident, your car insurer may pay for your damages first and then get reimbursed from the other driver’s insurance.

Why These Terms Matter

Knowing these terms helps you:

- Understand what you’re really paying for

- Avoid hidden costs or coverage gaps

- Compare policies more accurately

- Communicate better with insurance agents

Insurance can be confusing, but once you grasp these key terms, you’ll be in control — not the other way around.