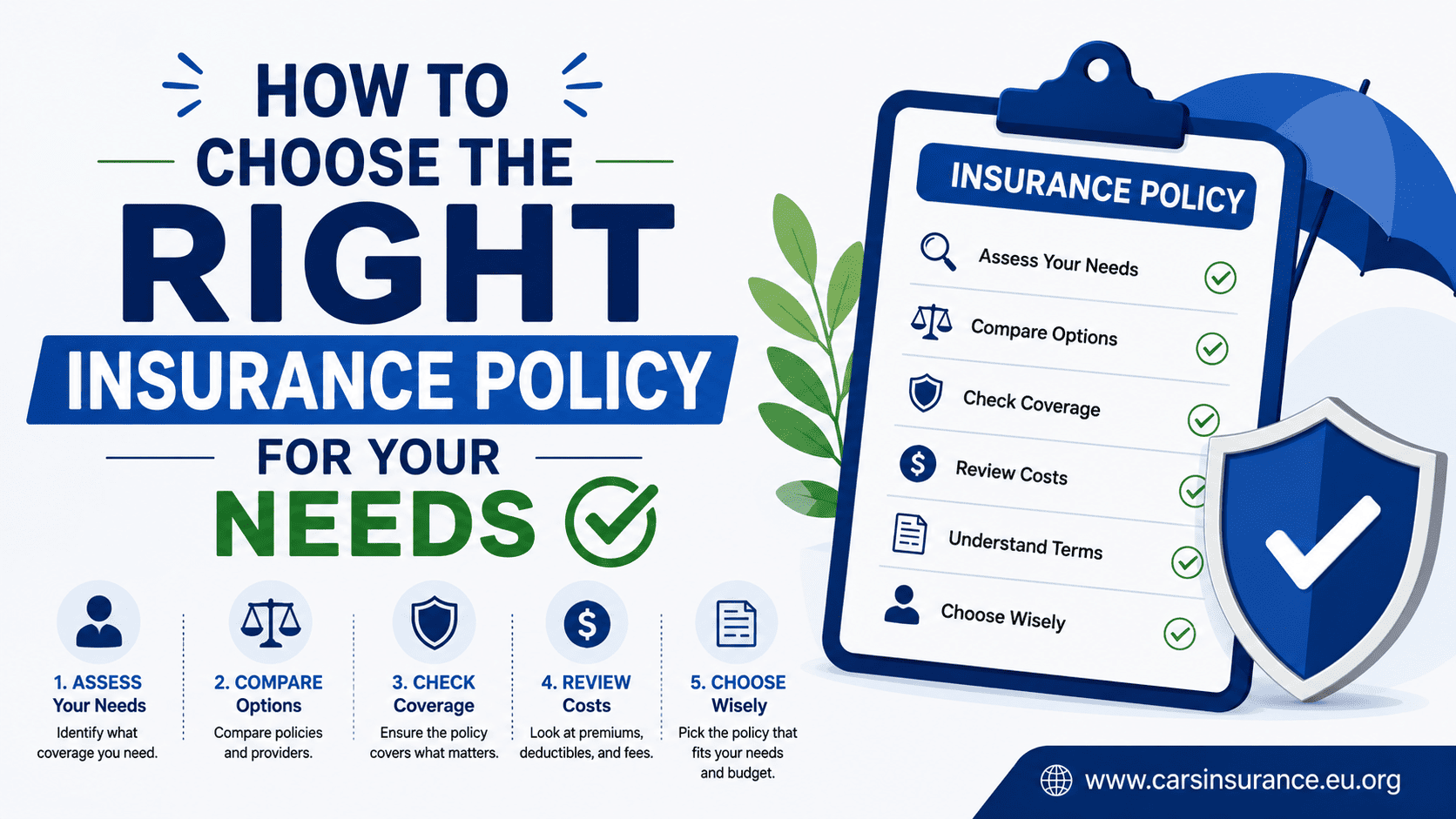

Buying insurance can feel overwhelming. With so many options, fine print, and confusing terms, how do you know which policy is truly right for you?

Whether you’re buying your first health plan, choosing life insurance for your family, or protecting your home or car, understanding how to choose the right insurance policy can save you money — and protect you from nasty surprises later.

In this guide, we’ll break down everything you need to know in simple, everyday language — so you can make confident, informed decisions about your coverage.

Why Choosing the Right Insurance Policy Matters

Insurance isn’t just another bill — it’s a financial safety net. The right policy ensures that when life takes an unexpected turn, you and your loved ones are financially secure.

Choosing poorly, on the other hand, could mean:

- Paying too much for coverage you don’t need

- Being underinsured when you actually face a loss

- Having claims denied because of exclusions or unclear terms

The goal is simple: get the right protection at the right price — not the cheapest, but the one that fits your situation best.

Step 1: Identify What You Need to Protect

Before you buy anything, ask yourself:

“What do I really need insurance for?”

Different people have different priorities. For example:

- If you’re single and healthy, health insurance might be your top concern.

- If you own a car or home, auto or homeowners insurance is essential.

- If you have a family, life insurance becomes critical.

- If you’re self-employed, you might also consider disability or business insurance.

Make a list of the biggest risks you face — illness, accidents, theft, property damage, or loss of income. That list becomes your insurance shopping checklist.

Step 2: Learn the Basic Types of Insurance

Here’s a quick refresher on the major types of insurance and what they cover:

| Type | What It Covers | Why It Matters |

|---|---|---|

| Health Insurance | Medical costs like doctor visits, hospitalization, prescriptions | Protects you from huge healthcare bills |

| Life Insurance | Provides money to your family after you pass away | Replaces income and supports dependents |

| Auto Insurance | Vehicle damage, theft, and accident liability | Legally required in most countries |

| Homeowners/Renters Insurance | Property loss or damage | Protects your home and belongings |

| Disability Insurance | Lost income due to illness or injury | Keeps money flowing if you can’t work |

| Travel Insurance | Trip cancellations, lost luggage, or overseas medical emergencies | Useful for frequent travelers |

You may not need them all, but understanding your options helps you focus on what’s most relevant.

Step 3: Understand Key Terms Before You Buy

Insurance policies are full of jargon. Knowing a few essential terms helps you compare plans accurately:

- Premium: The amount you pay (monthly or yearly) for coverage.

- Deductible: The amount you pay out of pocket before insurance kicks in.

- Coverage Limit: The maximum amount the insurer will pay for a claim.

- Exclusions: Situations or conditions not covered by your policy.

- Copayment / Coinsurance: Your share of costs for certain services (common in health insurance).

👉 Pro Tip: A lower premium usually means a higher deductible — and vice versa. Choose based on your risk tolerance and financial comfort.

Step 4: Compare Multiple Policies

Never buy the first policy you see. Insurance companies vary widely in what they offer, even for similar coverage.

Here’s how to compare effectively:

- Use official and trusted comparison tools.

- In the U.S., visit Healthcare.gov for health plans.

- For auto or home insurance, you can use NAIC’s tools or comparison sites like NerdWallet and Policygenius.

- Check coverage details, not just price.

A cheap plan might exclude key protections (like out-of-network doctors or flood damage). - Read customer reviews and complaint ratios.

The National Association of Insurance Commissioners (NAIC) tracks complaints for each insurer — a good indicator of reliability. - Ask questions before you buy.

If something’s unclear, talk to an agent or customer support. Don’t sign until you fully understand what you’re getting.

Step 5: Choose the Right Coverage Amount

Too much coverage wastes money; too little coverage leaves you exposed. The trick is finding the balance.

Here are a few quick guidelines:

- Life Insurance: Aim for at least 10–15 times your annual income (depending on debts and dependents).

- Health Insurance: Choose a plan that fits your typical medical needs — if you rarely go to the doctor, a higher deductible plan may save you money.

- Homeowners Insurance: Insure your property’s replacement cost, not just its market value.

- Auto Insurance: Get enough liability coverage to protect your assets in case you cause an accident.

If you’re unsure, an independent insurance advisor (not tied to one company) can help calculate the ideal coverage level.

Step 6: Check the Company’s Reputation and Financial Strength

Your insurance is only as good as the company behind it.

Look for insurers that are financially stable and known for paying claims promptly. You can check their ratings at:

Avoid companies with unclear claims processes, poor customer service, or a history of denying legitimate claims.

Step 7: Read the Fine Print Carefully

This step is often skipped — and it’s where most people get into trouble.

Always review your policy document before signing. Pay special attention to:

- Exclusions: Common examples include pre-existing conditions, acts of war, or intentional damage.

- Claim procedures: Know what documentation is needed to file a claim.

- Renewal terms: Some policies renew automatically; others require manual renewal.

- Cancellation clauses: Understand how to cancel or change your policy without penalties.

If any term is unclear, ask for a plain-language explanation. Insurers are legally required (in most countries) to help customers understand their contracts — see the Consumer Financial Protection Bureau (CFPB) for guidance.

Step 8: Review and Update Your Policies Regularly

Your life changes — and so should your insurance. Review your policies at least once a year or after major life events, such as:

- Marriage or divorce

- Buying a new home or car

- Having children

- Changing jobs or income level

Updating your coverage ensures you’re neither overpaying nor underprotected.

Step 9: Consider Bundling or Discounts

Many insurers offer bundle discounts if you buy multiple policies (for example, auto + home insurance). You can also save by:

- Installing security systems at home

- Maintaining a good driving record

- Paying annual premiums instead of monthly

- Completing health or wellness programs (for health insurance)

Ask your insurer about all available discounts — they can add up to substantial savings over time.

Final Thoughts

Choosing the right insurance policy isn’t about luck — it’s about understanding your needs, comparing options, and reading carefully.

Take the time to:

- Identify your risks

- Learn key terms

- Compare several providers

- Read the fine print

Insurance might not feel exciting, but it’s one of the smartest financial decisions you’ll ever make. With the right policy, you’re not just protecting your assets — you’re protecting your peace of mind.

Remember: good insurance feels unnecessary until the day you need it.