If you’re in your 20s or 30s, chances are you’re focused on building your career, saving for travel, or paying off student loans — not on buying insurance. Many young adults think insurance is something to worry about “later in life.”

But here’s the truth: the earlier you get insurance, the better.

Life is full of surprises — and not all of them are good. An unexpected accident, illness, or loss could drain your savings in an instant. Insurance is not just for the old or wealthy; it’s a smart financial move for anyone who wants to stay protected and independent.

In this article, we’ll explore five major reasons why getting insurance while you’re young can actually save you money, protect your goals, and set you up for long-term financial success.

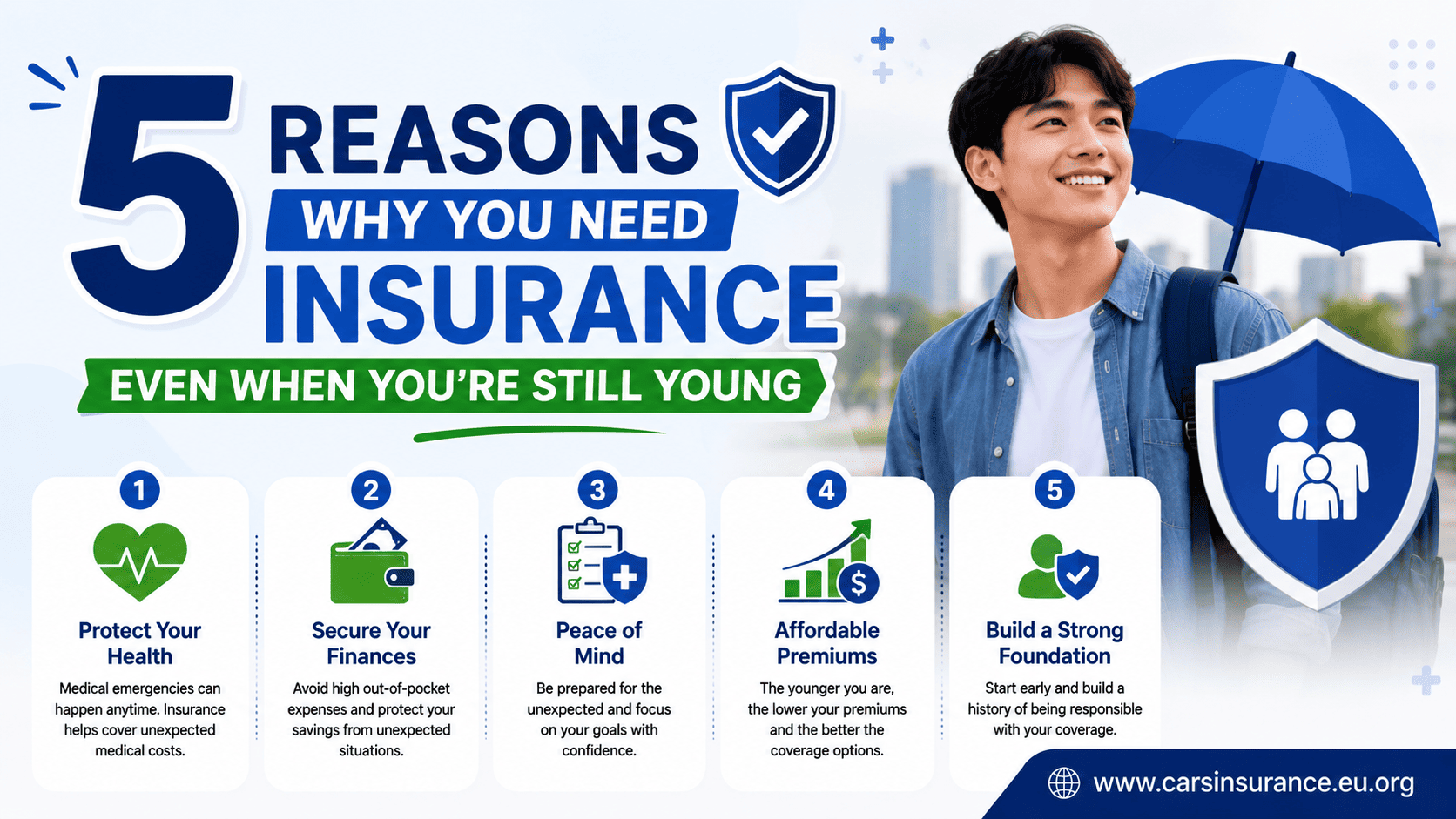

1. You Get Lower Premiums When You’re Young

One of the biggest advantages of getting insurance early is lower cost.

Insurance premiums — especially for life and health insurance — are heavily based on age and health condition. Younger people are generally healthier and less risky for insurance companies, which means you’ll pay significantly less for coverage.

For example:

- A healthy 25-year-old might pay around $20–$30 per month for a term life policy worth $250,000.

- The same coverage for someone aged 40 could cost three times more.

The same logic applies to health insurance. If you’re under 30, you may qualify for lower-cost “Catastrophic” plans on HealthCare.gov.

In short: the earlier you buy, the more affordable your protection — and those savings can last for decades.

2. Medical Emergencies Can Happen Anytime

Many young people believe they don’t need health insurance because they’re healthy and rarely see a doctor. Unfortunately, accidents and sudden illnesses don’t check your age first.

A single trip to the emergency room can cost thousands of dollars — and if you need surgery or hospitalization, the bill can skyrocket.

Here are some examples:

- A broken leg can cost over $7,500 to treat.

- Three days in the hospital might cost $30,000 or more.

(Source: Healthcare.gov)

Without insurance, these costs can easily drain your savings or push you into debt.

Health insurance not only covers emergencies — it also helps pay for preventive care like vaccinations, annual checkups, and screenings. These small steps can prevent larger (and more expensive) problems later.

So even if you’re young and healthy, insurance protects you from the unpredictable.

3. Your Income Needs Protection Too

Think about it: your income is your most valuable asset right now. You depend on it to pay for rent, food, bills, and your lifestyle. But what if you suddenly couldn’t work due to an accident or illness?

That’s where disability insurance comes in.

Disability insurance replaces a portion of your income if you can’t work for medical reasons. Even short-term disabilities (like a back injury or long recovery after surgery) can seriously affect your finances.

According to the Social Security Administration, 1 in 4 people who are now 20 years old will become disabled before they reach age 67.

If your employer offers disability coverage, that’s great — but if not, you can get an individual plan. It’s one of the smartest financial protections you can have, especially early in your career.

4. Insurance Helps You Build Financial Discipline

Insurance isn’t just about emergencies — it’s part of a financial plan.

Paying premiums regularly teaches you to manage your money and think long-term. It’s a form of forced saving that builds responsibility and awareness of your financial priorities.

Some types of insurance, like whole life insurance, even have a savings or investment component. You can borrow against its cash value later for big goals like buying a house or starting a business.

It’s not about the product itself — it’s about developing healthy financial habits while you’re still young enough to make them stick.

Pro Tip:

When you budget for essentials like rent, food, and transportation, treat insurance premiums as a non-negotiable expense. That mindset keeps you protected without stress.

5. Life Changes Faster Than You Think

When you’re young, life feels open and flexible — but things can change quickly. You might get married, start a family, buy a car, or purchase your first home.

Each of these milestones increases your financial responsibilities — and the need for insurance.

- Getting married? You now share financial obligations. Life insurance can protect your partner.

- Buying a house? You’ll need homeowners insurance (often required by lenders).

- Having kids? Life and health insurance become non-negotiable.

- Starting a business? You’ll need general or business insurance to protect your income source.

By getting coverage early, you’re already prepared for these transitions. Plus, you can often add or upgrade your policies easily as your life evolves.

Bonus: You Protect Your Family Too

Even if you’re single and independent, your family may rely on you in small but important ways — like helping with bills, sending money home, or sharing rent.

If something unexpected happened to you, life insurance ensures they’re not left struggling financially.

It’s not just about leaving a legacy — it’s about showing care and responsibility. For many young adults, that’s the first big step toward financial maturity.

Common Myths Young People Have About Insurance

Let’s clear up a few popular misconceptions:

- “I’m too young for life insurance.”

→ Actually, this is the best time. Premiums are lowest when you’re young and healthy. - “Insurance is too expensive.”

→ In most cases, basic health or term life coverage costs less than a few streaming subscriptions per month. - “I don’t have dependents, so I don’t need insurance.”

→ You still have income, bills, and future plans to protect. - “My job covers everything.”

→ Employer coverage often ends when you switch jobs. Having personal policies ensures you’re always protected.

How to Get Started

If you’re new to insurance, here’s a simple checklist:

- Start with health insurance.

It’s the most critical protection for your physical and financial health. Compare plans on Healthcare.gov or through your employer. - Add life insurance if you have dependents or debts.

A term life policy is affordable and simple. Learn more at the Insurance Information Institute (III). - Consider disability or renters insurance.

If you rent your place or rely on your income (which most of us do), these are worth it. - Review your coverage yearly.

Life changes — your insurance should evolve too.

For trustworthy comparisons and consumer advice, visit the National Association of Insurance Commissioners (NAIC) or the Consumer Financial Protection Bureau (CFPB).

Final Thoughts

Getting insurance while you’re young might not feel urgent — but it’s one of the smartest financial decisions you can make.

It’s not about expecting bad things to happen. It’s about being prepared if they do.

By locking in low premiums, protecting your income, and developing good money habits early, you set yourself up for financial stability that lasts a lifetime.

So don’t wait until something goes wrong — start protecting your future today.