Insurance can be confusing — especially when you’re just starting to manage your personal finances. You hear about life insurance, health insurance, and something called general insurance, but how do they really differ? And which one should you prioritize first?

If you’ve ever wondered how these types of insurance work and why they’re all important, this guide is for you. We’ll explain the basics in plain English, give real-world examples, and help you understand how to protect yourself financially.

Why Insurance Matters in the First Place

Before diving into the differences, let’s start with the big picture.

Insurance is a safety net. It’s there to protect your money when life throws unexpected events your way — illness, accidents, property damage, or even death.

Instead of paying huge amounts out of pocket, you pay a smaller, regular amount called a premium. In exchange, the insurance company covers certain risks defined in your policy.

In short:

Insurance transfers financial risk from you to the insurer.

But since there are different risks in life — from getting sick to losing your house — we have different kinds of insurance. The three most common categories are life insurance, health insurance, and general insurance.

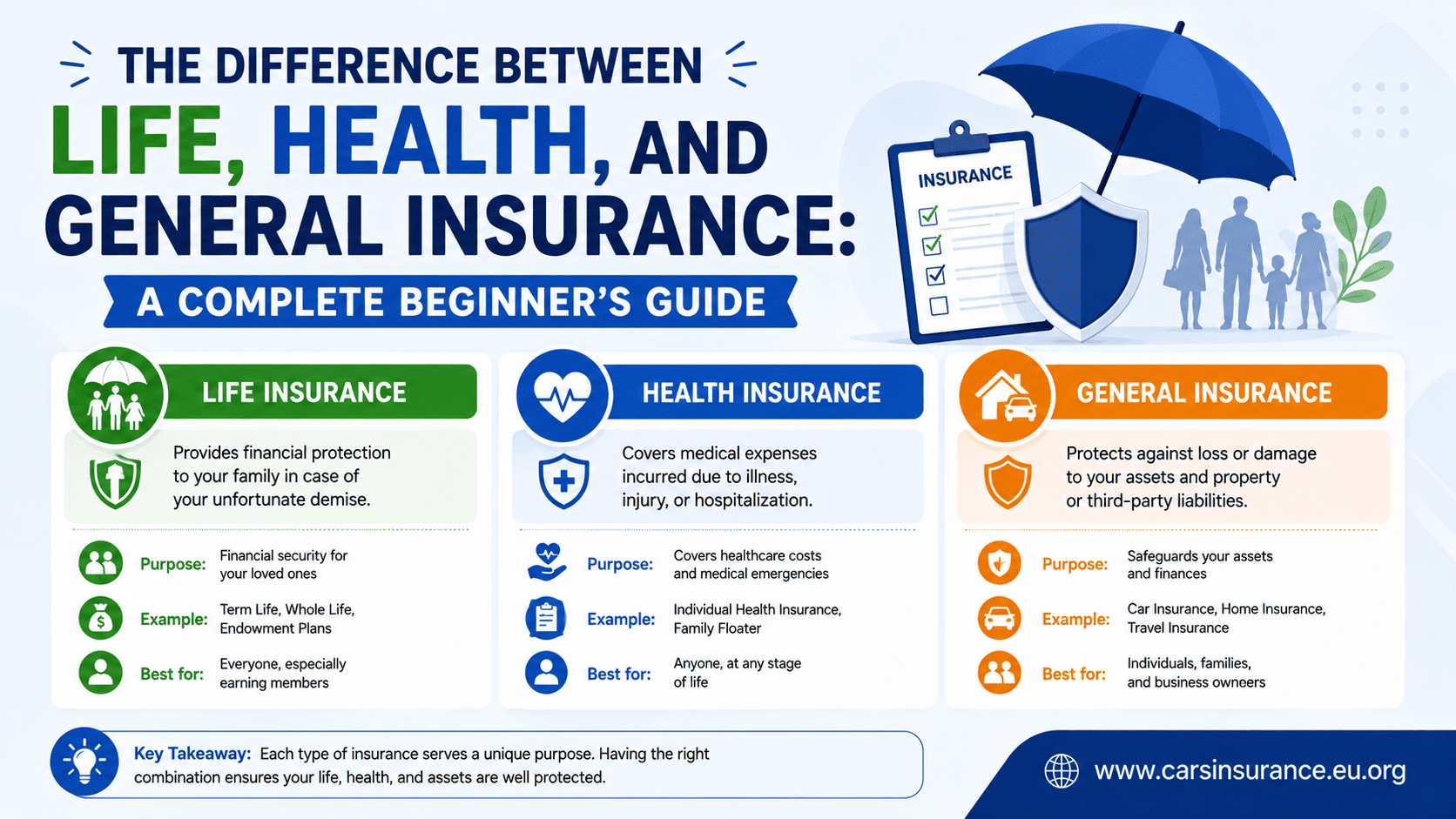

1. Life Insurance: Protecting Your Family’s Future

What It Is

Life insurance provides financial protection for your loved ones if you pass away. When you die, your beneficiaries (like your spouse, children, or parents) receive a lump sum payment, known as a death benefit.

It’s meant to replace your income, pay off debts, or cover future expenses such as your children’s education or mortgage.

Types of Life Insurance

There are two main kinds:

- Term Life Insurance – Coverage for a specific period (like 10, 20, or 30 years). If you pass away during that term, your family gets the payout. It’s affordable and straightforward.

- Whole or Permanent Life Insurance – Coverage that lasts your entire life and often builds cash value that you can borrow from. It’s more expensive but includes a savings component.

Why It Matters

If someone depends on your income — like your partner, kids, or aging parents — life insurance is essential. It gives them financial stability even if you’re no longer around.

According to the Insurance Information Institute (III), life insurance can also help with estate planning, taxes, and business continuity.

Example

Let’s say you earn $50,000 a year and have two young children. If you unexpectedly pass away, life insurance ensures your family can still pay the bills, keep their home, and continue their education.

2. Health Insurance: Covering Your Medical Costs

What It Is

Health insurance helps you pay for medical expenses such as doctor visits, hospital stays, surgery, and prescriptions. It can also cover preventive care like vaccines and screenings.

In the U.S., health insurance is often provided through employers, private companies, or government programs like Medicare and Medicaid.

How It Works

You pay a monthly premium, and in return, the insurance company covers part or all of your medical bills. Depending on your plan, you may also pay:

- Deductible: The amount you pay before your insurance starts covering costs.

- Copayment: A small fee for each visit or prescription.

- Coinsurance: A percentage of the bill you’re responsible for after the deductible.

Why It Matters

Healthcare can be incredibly expensive — a single hospital stay can cost thousands of dollars. Without insurance, medical bills can quickly lead to debt or bankruptcy.

As Healthcare.gov notes, even healthy people benefit from insurance because it gives access to preventive services that keep you healthy long-term.

Example

If you break your arm, treatment could cost $7,500 or more. With insurance, you might pay only a few hundred dollars, and the insurer covers the rest.

3. General Insurance: Protecting Everything Else

What It Is

While life and health insurance cover your life and well-being, general insurance covers everything else — like your car, home, travel, or business.

It protects you from losses due to accidents, theft, natural disasters, or liability claims.

Common Types of General Insurance

- Auto Insurance: Covers damage to your car and liability if you cause an accident. Required by law in almost every U.S. state. (See USA.gov’s car insurance guide)

- Homeowners Insurance: Protects your house and belongings from fire, theft, or disasters. Lenders usually require it.

- Renters Insurance: Covers your personal items if you rent an apartment.

- Travel Insurance: Helps if your trip is canceled, delayed, or if you get sick abroad.

- Business Insurance: Covers companies from risks like property damage or employee injuries.

Why It Matters

General insurance provides peace of mind and financial recovery when unexpected events happen. Imagine losing your home to a fire or getting into an accident — these are life-altering situations.

Without insurance, you’d bear all the financial losses yourself.

Key Differences Between Life, Health, and General Insurance

Here’s a simple comparison to make things clearer:

| Feature | Life Insurance | Health Insurance | General Insurance |

|---|---|---|---|

| Purpose | Protects family after death | Covers medical expenses | Protects assets & property |

| Duration | Long-term or lifetime | Annual (renewable) | Usually annual |

| Benefit Type | Lump-sum payment after death | Payment/reimbursement of medical bills | Compensation for specific loss |

| Who Benefits | Dependents or nominees | The insured person | The insured person or asset owner |

| Examples | Term life, Whole life | PPO, HMO, Medicare | Car, home, travel, business |

Understanding this table helps you see how each one plays a unique role in your overall financial protection plan.

How to Choose the Right Mix of Insurance

Choosing the right coverage depends on your life stage, income, and personal situation. Here’s a quick guide:

- Young professionals: Focus on affordable health insurance and maybe term life if you have dependents.

- Families: Consider comprehensive health coverage, life insurance, and homeowners or auto insurance.

- Business owners: Add general business insurance and disability coverage.

- Retirees: Prioritize health and life insurance to secure medical needs and family support.

The National Association of Insurance Commissioners (NAIC) offers tools and consumer tips to compare policies and understand your state’s regulations.

Common Mistakes to Avoid

- Only buying insurance because it’s cheap.

Low premiums often mean limited coverage. Always read the fine print. - Not updating your policies.

Major life changes — marriage, kids, home ownership — should trigger a review. - Ignoring general insurance.

Many people protect their health and life but forget about their home or vehicle, which can be just as costly to replace. - Relying only on employer coverage.

If you change jobs or lose your job, your coverage may end. Always have a backup plan.

Final Thoughts

Insurance might not be the most exciting topic, but it’s one of the smartest financial decisions you can make. It protects your health, your loved ones, and everything you’ve worked for.

To sum it up:

- Life insurance protects your family’s future.

- Health insurance protects your well-being.

- General insurance protects your assets.

Each serves a different purpose, but together they form the foundation of a solid financial plan.

Take a few minutes today to review what coverage you have — and what you might still need. You’ll thank yourself later when life’s surprises come your way.